Did we just open Pandora's box?

Weekly Credit Review 26.09-30.09

This week the FED reinforced their commitment to keep rates higher for longer. From 2008 until 2022 we witnessed a prolonged period of ultra low rates which triggered an immense speculation in both stocks and real estate. The last 2 years in particular marked a blow off top in valuations in equities and real estate. I have a strong feeling we will not see these highs for quite some time.

14 years seems like just enough time to rewire the brains of a whole generation of traders that were conditioned to buy any dip because the FED would always be there or simply because we were in a decade long bull market. Now your savior had turned into your worst nightmare. Mr. Powell said multiple times that it is the FED’s mission to kill inflation and they are ready to do what it takes to get there. Would I want to invest in such an environment, hell no! Would I do short-term long trades, hell yes! In the next 9-12 months a lot of freshly minted traders and investors would realize that long-only strategies do not work as well in volatile markets. Breakouts, buying the dip and valuation strategies will cease to work until a bull market is upon the horizon again. But I don’t see how we get a prolonged bull market given we have not even entered recession yet and unemployment is still as strong as it has ever been. There is plenty of time until investing becomes fashionable again.

On the bright side, we are now entering an exceptionally good environment for short-term traders. Should volatility pick up further we will see an influx of mispriced corporate credit, ETFs , stocks and of course exceptionally expensive options which would be great to short.

WHAT HAPPENED LAST WEEK?

iTraxx Crossover and iTraxx Europe marked new yearly highs. Hope you like volatility. Active European credit traders will see a lot of opportunities coming their way this year.

SPX is at the Jun’22 lows. I am not sure we break the lows next week, but given the FED’s stance I expect the next few weeks to be very volatile, eventually leading to a break down in SPX. This will translate to widening credit spreads in both investment grade and high yield bonds.

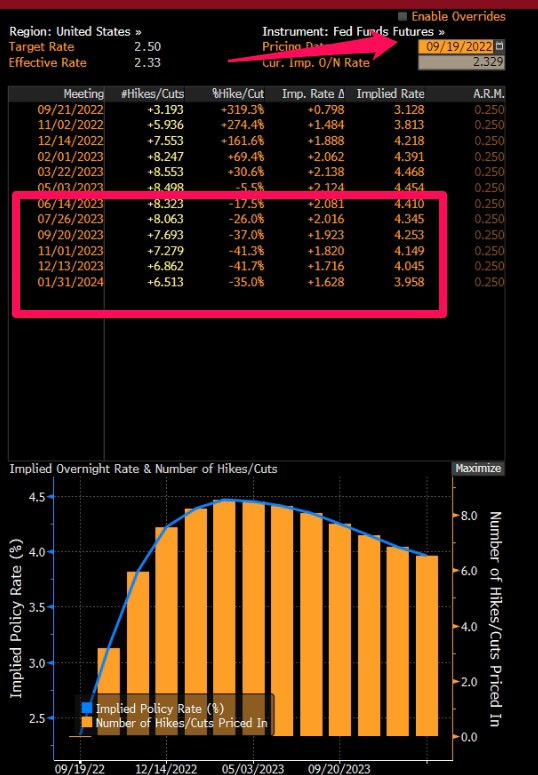

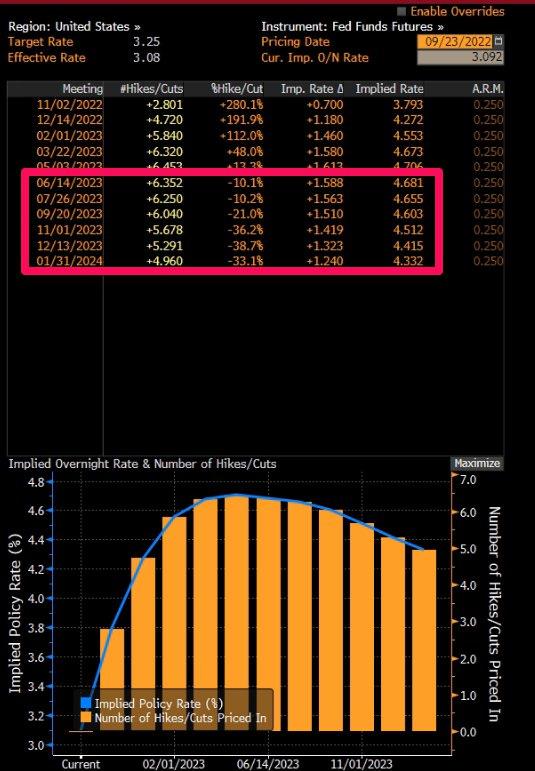

The market priced in 25bps in less rate cuts in the end of ‘23 and ‘24. Talk about higher for longer. Should we get another higher than expected CPI report I expect to see an even flattish curve until the beginning of ‘24.

My main thesis for the next few weeks will be to wait for a bounce which I could use for building new short positions. As I am reluctant to short at the lows I will try to remember how important patience is and the fact that it is patience that makes the big bucks for traders. Alternatively, if we don’t see a bounce, we will have to wait for a selling exhaustion or capitulation and go long then, but I think we are not close to such a condition yet. We need the VIX above 40.

POTENTIAL POSITIONS:

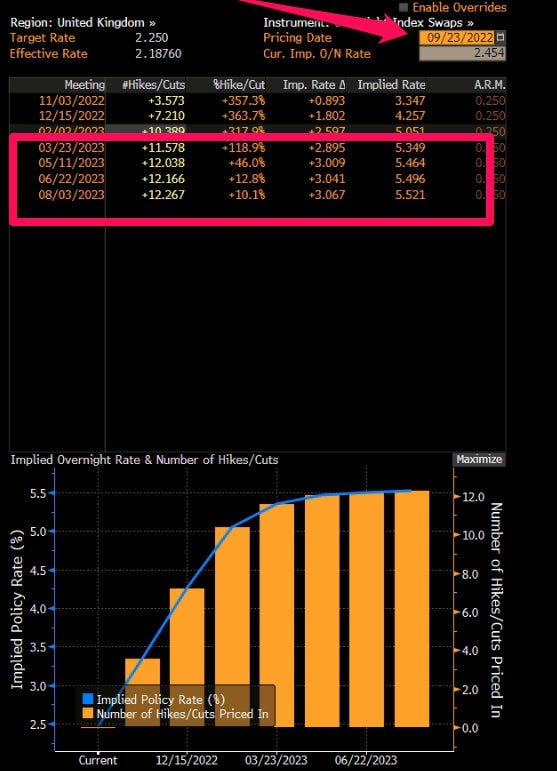

On Friday we all saw what happened in the UK. Short-term yields sky rocketed. The GB02Y and GB05Y were up by 0.32bps and 0.49bps respectively. You don’t need to be told this is an exceptional move, especially for a bond market. I view this as a step closer to building a blow off top in UK yields and am on the lookout to buy GILTS. Ideally I would want to see 1-3 days more of such activity. It is worth mentioning that this suggestion is a short-term trade rather than an investment into British bonds. If timed correctly it can take from 1-3 days to work out. This is far from having a long-term view on the British economy.

My trigger will be either the UK OIS curve begging to easy or the yield reaching the levels that the UK OIS curve is currently pricing. As of this writing March’23-Aug’23 OIS curve is pricing roughly 6% rates. That is quite the move from just a few days ago when rates were at 5.5%. That is a few days, not months. You don’t get to see that volatility in a developed market’s bonds every day.

HYGH - This ETF shows you the credit spreads of US high yield bonds. The lower it goes, the wider the spreads are, the higher it goes, the tighter spreads are. My bet is HYGH goes lower from here but as I don’t believe shorting at the lows makes for a great risk to reward trade I am hoping for a bounce to the $82 level to initiate a short.

VNQ - As in the HYGH suggestion, I am hoping for a bounce to $87.50ish to initiate a short position. In fact most ETFs and credit looks similar to the VNQ chart and the best course of action right now will be to wait for a bounce. Assuming we get there I am going to get 1 month ATM call and short the underlying, a position known as synthetic put.

CURRENT POSITIONS:

MET-F vs MET 3.85 1x2 notional exposure.

PGX vs WFC 5.875 0.5 vs 2x notional exposure. This is basically short WFC 5.875 while I cashed in partial loss in PGX as I am bearish and prefer to only leave the short position.

We booked profits in REM last week and we are left with 1/3 of the initial position size.

MAJOR RISKS:

The start of earnings season my push stocks further to the downside, should we get more revise guidance and grim forward outlook from multiple companies.

Stress from the UK and EU’s bond markets spreading to the US. The UK’s OIS curve is pricing 6% rates in the spring of 2023. Just one week ago the UK was pricing 5.5% in rates in the spring of 2023. That is a huge repricing, no wonder we saw quite the explosion in British yields. The EU is currently sitting at 3% but it is very likely we keep on marching higher.

CONCLUSION:

Central banks had been very active last week and all signaled higher terminal rates and for longer. There is no way this is bullish for the equity markets. Until this view changes I focus on doing 2 things:

Look for capitulation in individual names and buy them for a very short-term trade.

Wait for a bounce to short sectors most affected by higher rates, such as real estate. The trade plan is buying ATM synthetic puts in the ETFs and symbols I follow closely. Examples are VNQ, REM. Additionally I am looking to short high yield corporate bonds of names most affected by higher rates. Again this includes VNQ and REM high yield names but this idea can be applied to any other sectors largely affected by what is going on.

I will NOT look for buying anything for the long-term no matter how good it looks. I want to emphasize that this is a trader’s market and we have not yet seen volatility pick up. I expect charts to get ugly in the near future. Stay safe and remember that risk management is what keeps us in the business. Being a hero is right now is not advisable.

SUGGESTED READING:

This new section will include the work of other authors who I enjoy reading and help me build an informed framework for the markets.

The Macro Tourist - posts.themacrotourist.com - Kevin has a knack for identifying opportunities that others rarely see. What makes his approach unique is his macro view which can translate into actionable swing trading ideas.

FX Macro - fxmacro.info - A an excellent overview of what happened in the world of FX and Central banking.

The Morning Hark - harkster.substack.com - A great way to start your trading day. You have a summary of what happened in most major markets.